The Permanent Growth Environment

And Its Effects on Us

This is a chapter from my book, Revamping the Permanent Growth Environment: How Good Strategy Beats Market Pressure, and reproduced here in this article. The full book is available for purchase on Amazon and Barnes & Noble.

Please enjoy and comment.

Chapter 1

The Permanent Growth Environment

The business environment plays as much of an important role in strategy formation and decision making as any factor we will discuss. Many scholars have shown that social context, societal factors, and environment will influence decision making. For example, people will want to fit with norms, favor the status quo, and select the default option through non-decision. Over time, those decisions stack up and legacies are created. These legacies become the foundations of cultures. This culture provides the menu of acceptable decisions and philosophical positions for people. In politics, this is called the Overton Window. And, in business, this effect is real, and it sets what is acceptable for business decision making.

There is a lot that goes into building the business Overton Window. First, the capitalist system. No matter the point of view, it cannot be understated the basic expectation of private property rights, especially those over profits, and the impact of having free markets. Preserving capitalism is often at the center of policy debates, and it filters into decisions at individual firms. The concept is built into core competitive concepts and key business metrics. As the old business axiom states, “what gets measured, gets done.” That applies no matter what expenditure being considered.

An extension of capitalism is shareholder primacy. Depending on the terminology and business type, shareholders, stockholders, or members (for simplicity, we will refer to them as shareholders going forward) own certain rights to a business’ profits and to vote on key matters, including the election of directors. It is generally accepted that shareholders believe their interest must come before the interests of any other stakeholder in the company, and their main interest is profit maximization. If profits are not maximized, then shareholders have the right and responsibility to smear the company in the media, sue the company, remove corporate officers, attempt a hostile takeover, or all of the above. This belief has only grown stronger as private equity funds, institutional shareholders, and activist shareholders have come armed with business metrics and plans focused on unlocking shareholder value.

Shareholders have reinforced this philosophy by applying the right incentives and pressures on corporate officers. Most directly is through executive compensation. It is commonly known and understood that stock awards, stock options, and other equity-based incentives add great wealth to the officers of the company. From 1978 to 2018, CEO compensation at the 350 largest publicly traded companies increased 940% with stock compensation as a main contributor. Stock compensation makes shareholders out of executives. Thus, in their view, any decision to abandon shareholder primacy is a limiter on maximizing their own wealth. For publicly traded companies, this means maximizing the stock price, which means taking actions that are generally accepted by Wall Street to unlock value (e.g., cost reductions, buybacks, etc.).

Debt can also reinforce the concept of shareholder primacy by establishing another type of primacy. After the Great Depression, people were leery about using debt. This was understandable since deflation makes it harder to pay debts, and deflation was rampant during the Great Depression. Those sentiments faded over time, but even a firm like the Boston Consulting Group had to work hard in the 1960s and 70s to convince businesses to increase financial leverage to gain market share.

Currently, corporate debt is at its highest levels in terms of total dollars and near all-time highs as a percentage of the gross domestic product. There are many reasons for this, but what follows are some of the bigger ones. For private equity, debt is used to purchase companies without committing too much shareholder capital and allows better returns. In certain situations, debt can be a positive market signal that a company is on a good course. Debt is also favored by management because it generally is a cheaper way to raise funds than issuing new shares and carries a lower cost of capital going forward. This lower cost of capital allows executives to approve more projects and investments, which can lead to higher and faster returns.

However, debt covenants can lead to strict financial management to stay ahead of certain bank requirements. For example, a bank can require a company to maintain certain financial ratios (e.g., debt-to-equity, current ratio, etc.) at a set amount and place restrictions on merger and acquisition activity and shareholder payouts. In some cases, debtholders will even have priority over the shareholders in a distribution of corporate profits and assets. This seemingly creates debtholder primacy. This combined shareholder and debtholder primacy provides the motivating basis for many corporate strategies and decision making. But, for the purposes for the rest of this book, we will refer to this collectively as shareholder primacy.

Another key business environmental factor is human nature. Corporate decision makers, whether they are CEOs, board members, or divisional presidents, are people. And people have needs. In this case, these people are securing the resources to feed their families, pay their bills, etc. Additionally, there are ambitions, reputations, commitments to culture, and many other personal considerations that can go into a business decision. The authors of Strategy Beyond the Hockey Stick: People, Probabilities, and Big Moves to Beat the Odds refer to this as the “social side of strategy.” They argue that this “social side of strategy” is a major contributing factor in preventing companies from making large bets that could vastly improve their performance.

The internal and personal stakes for corporate decision makers cannot be understated. Annie Duke explains in her book Thinking in Bets: Making Smarter Decision When You Don’t Have All the Facts that the net effect of the biases, cognitive distortions, and other personal needs is motivated reasoning. In short, you are the protagonist of your own story. Anything that complicates or challenges that position will be rejected. Simply put, you are motivated to reason yourself to a position where your viewpoint is confirmed. Once you attach pecuniary interests to this motivated reasoning, then you can see how correct Upton Sinclair was when he wrote, “it is difficult to get a man to understand something, when his salary depends on his not understanding it.” While capitalism, shareholder primacy, and human nature seem like an exhaustive list in explaining the decision-making context in business, we will see that politics and time pressures play a key role as well.

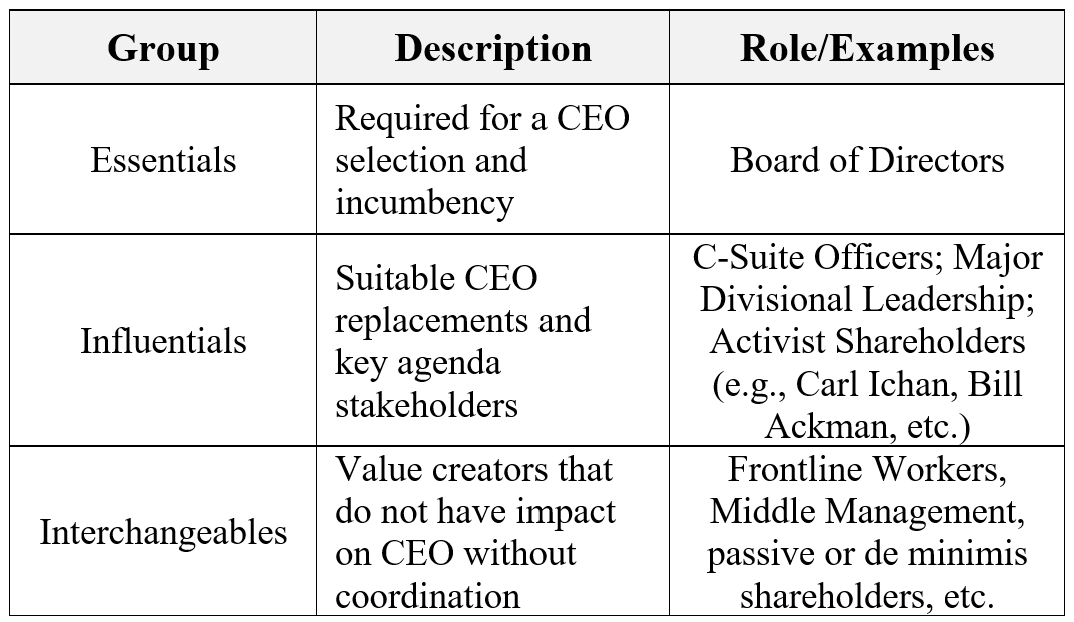

Politics is a consistent corporate topic. Colloquially speaking, we have all heard “I can’t believe [x] got a promotion, they must be good at politics.” Or “I really want to leave this company because everything is way too political here.” Well, unfortunately, everything is political everywhere, especially in business. For our purposes, we will use the framework laid out in The Dictator’s Handbook: Why Bad Behavior Is Almost Always Good Politics to better understand the role of politics in business decisions, and I will bet that you already understand these factors intuitively. In The Dictator’s Handbook, the authors show how classical political naming conventions like monarchy, democracy, dictatorship, etc. are, in fact, descriptions of the relationship and relative size of three groups key to selecting and retaining a political leader. These groups are called the Interchangeables, Influentials, and Essentials. The Interchangeables can have some surface level say in picking leaders but do not wield any actual power. Interchangeables’ impact on leadership comes from their sheer numbers and ability to produce economic output. Leaders often prevent Interchangeables from coordinating to suppress the impact of their numbers. Influentials have direct impact on who is chosen as leaders by holding key positions and being available alternates for leadership. Essentials are a subset of Influentials who basically have the final say on who the leader will be.

In a corporate setting, CEOs lead companies and are selected by the board of directors. The board itself is elected by the shareholders. In The Dictator’s Handbook framework, Interchangeables are the frontline workers and up to its middle management. These groups can have nominal stakes but have no real ability to pick a slate of directors and get them elected or pick the CEO. The Influentials, on the other hand, can be senior executives, institutional investors, potential acquirers, high-profile analysts, and bankers, all of whom can be board members, alternative CEO candidates, or outside power brokers. Senior executives within a company are extremely key stakeholders in executing a CEO’s agenda and protecting their incumbency. However, those executives are also potential CEO replacements, if they get the opportunity to offer better business plans to the board. But unless they have board positions, they are not Essentials. Corporate boards vote directly on CEOs and their compensation, and, therefore, no one can be CEO without board support. Therefore, they are the Essentials. This is all summarized in Exhibit 1.

Exhibit 1

Here is the most intuitive part as suggested by The Dictator’s Handbook: CEOs must use company resources to enrich Essentials to gain and maintain power. If too much money is invested in long-term strategies or focused on improving the lives of the Interchangeables (i.e., employee compensation, benefits, workplace safety, etc.), then there will not be enough resources to keep the board happy. The board itself will generally have stock awards for themselves, and thus, they become tightly aligned with shareholder primacy. The CEO must also ensure the flow of money to other senior executives. This will ensure loyalty, peak execution, and prevent any executive from trying to take over the CEO role prematurely. Furthermore, the book suggests that because the number of Essentials is small, then, by structure, companies are dictatorships. The larger the number of Essentials the more democratic in structure a governing body will be. As a result, benefits, resources, and accountabilities flow to more people. But, in a small coalition of Essentials, only a few need to be consistently enriched, which incentivizes only giving the minimum number of resources and benefits to Interchangeables to keep them productive, not necessarily happy and stable.

This is clearly a cold analysis of the corporate structure. While the corporate structure matches that of small Essential group governing bodies, like monarchies and dictatorships, not all CEOs are power hungry and evil dictators, and I would not make such a broad personality assertion without better evidence. However, this structure certainly impacts corporate decision making. By structure, there will be few repercussions for CEOs making decisions that only enrich the board. Interchangeables and Influentials can only hold CEOs accountable in ways that do not necessarily impact the CEOs’ incumbency. Interchangeables can and do leave when enough disagreements with leadership mount, but, due to the fungibility of most roles, they are, as the name suggests, replaceable. In addition, the obstacles to unionization greatly diminish the ability for collective action to create more accountability for CEOs. Influentials can only create accountability with great personal or financial risk. Yes, an outside investor can start a proxy fight, but that is expensive and is likely to end with a settlement and board seat, which makes them one of few Essentials and not necessarily guaranteed to change a CEO. And while senior executives can make a play for the CEO position with the board, it is not likely to be successful, and that person’s ethics and loyalty will forever be in question. Such questions will disqualify that leader in other ventures and opportunities. Therefore, they can only do it if they know for a fact that they are going to win. As it was famously said on the show The Wire, “you come at the king, you best not miss.” As a result, an intuitive but understated aspect of strategic decision making is the unchecked and plenary power of the CEO that can successfully enrich the right people but not all people.

Lastly, we will discuss time pressures. This is the most straightforward of them all, and it works in two aspects. We all know that many businesses operate quarter to quarter. It is such a ubiquitous concept that it seems to have been around forever. In the United States, securities laws require that public companies report results on a quarterly basis, and analysts build expectations on those quarterly reports. If you beat the quarterly expectations, stock price and equity-based compensation increases. If you do not, then you need a really good excuse or be prepared to face calls for change from Wall Street and the board. There are also pressures from the passage of time. Every business model matures and that means every business model slows and produces growth at a slower rate. Bain partner Chris Zook describes this in his Focus-Expand-Redefine framework. McKinsey implores leaders to start preparing for that day in their Three Horizons framework. It is mathematically shown in Prof. Ghemawat’s Strategy and the Business Landscape by highlighting how performance and superior competitive position inevitably reverts over time. But leadership tends to only feel existential dread at business model maturity as it can be a limiter on growth and stock price (i.e., personal wealth). Therefore, depending on where your business is in the life cycle, corporate leaders could face delivering stronger than ever quarterly growth even though time and, in some ways, math works against them. This can lead to even more desperate decision making and more danger to Interchangeables.

In sum, capitalism provides a baseline philosophical and economic view to create what is acceptable options in a certain range of business activity in the United States. Shareholder primacy bolts on the idea that the enrichment of the shareholders is the top corporate priority to that economic thinking. The prevalence of share-based compensation reinforces shareholder primacy into the corporate political structures, where CEOs rule at the mercy of boards of directors and at some expense to everyone else. On top of this, human nature will further limit the number of overall options and favor picking options that are comfortable in some way rather than new alternatives regardless of merit. All of this plays out in a quarter-to-quarter accountability system that demands growth in stock price and wealth no matter where the company is in its strategic life cycle. This is the context for corporate decisions on everything in a company from strategy to worker treatment to selecting a janitorial service vendor, et. al. We will now refer to this as the Permanent Growth Environment.

The Effects of the Permanent Growth Environment

The Permanent Growth Environment requires solutions or growth plans to be identified, solved, and returning maximized profits within three months. Any option that does not fit that criterion will not be seriously considered or implemented. It will be considered next quarter’s, next year’s, and maybe the next owners’ problem. If companies complete a strategic process that presents a robust and well-founded strategy, the temptation for short-term maximization can lead to gutting those plans or reshaping them in some way to meet the earlier criterion. For a lot of companies, they will skip or never consider studying their competitive positions, value proposition, key trends, or other factors at all. The process would be too slow to get maximized profits next quarter. “We must act now” or “move fast and break things” is what they preach to convince themselves they are on the right track. Consulting firms can offer quick study and robust solutions, but that is expensive and requires people to focus on something other than everyday work. Thus, consultants will get ruled out, brought in on limited scope, not listened to, or brought in only when the situation is extremely bad.

The Permanent Growth environment not only provides criterion for strategic options during decision making but also limits possible solutions. In my experience, “field of dreams” strategies are generally left to venture capital and entrepreneurship even though more mature companies will wish they had the entrepreneurial spirit themselves. The Permanent Growth Environment will limit the questions you can ask about your company and the market overall. Concepts will not be explored because from the outset only one answer will meet the criterion. Automatically, the strategic solution set available will be limited to buying growth through mergers and acquisitions, selling more of what you already sell, or creating cost efficiencies, often by cutting people and benefits.

Companies will continue to select from limited strategic solutions over and over again. If decisions do not work, the solution set itself will narrow over time. This means the ability to fix problems gets narrower and narrower until the fundamentals of the company are completely broken. Upper leadership will get fired, and new leadership, often with consulting help, will go for a complete revamp by re-opening the strategic set and, unfortunately, likely to start this process all over again but from a different basis. Along the way, companies will cause unemployment, ignore or exacerbate social ills, and, in some cases, put people at risk with their products.

Therefore, the Permanent Growth Environment is overall just a limitation on what we can accomplish in companies, and the impacts are felt in both the company and society. It is a rare day, usually after a change in leadership or in a pure venture setting, that the full strategic solution set is truly considered, weighed, and acted upon no matter where the truth takes leadership. Understanding this environment is the first step in building better corporate decisions and pushing decisions that benefit more people. In the next two chapters, we will look in depth at the decision categories to avoid while operating in the Permanent Growth Environment and the legacy of those decisions.